- BettingStartups News

- Posts

- Waterhouse VC: Castles with Moats

Waterhouse VC: Castles with Moats

This month, Tom Waterhouse explores the concept of “moats” and why Evolution stays ahead.

Tom Waterhouse

March 31, 2026

Every month, industry investors Waterhouse VC publish an article that spotlights different aspects of the ecosystem. This month, Tom Waterhouse explores the concept of “moats” and why Evolution stays ahead.

In an era where artificial intelligence is eroding software advantages faster than ever, the strongest moats are increasingly built on physical infrastructure, regulatory complexity and hard-won trust. Evolution is one of the clearest examples of that in wagering. The Stockholm-listed company (ticker: EVO) supplies live casino games and digital content to online gambling operators.

“A good business is like a strong castle with a deep moat around it. I want sharks in the moat. I want it untouchable.” - Warren Buffett

When we profiled the company in June 2022, revenue had passed €1 billion and the company was running 15 studios for over 600 customers. In 2025, it generated €2.07 billion in net revenue across 24 studios in 16 jurisdictions with an adjusted EBITDA margin of 66.1%. Yet the stock has fallen sharply as regulatory pressure, operational setbacks and back-to-back year-on-year quarterly revenue declines have weighed on sentiment. The business underneath has not changed nearly as much as the price.

Structural Tailwinds

Consumer attention is moving to video. Reels account for roughly 50% of time spent on Instagram. Live casino rides the same shift and is already mobile native, with 71% of Evolution’s 2024 revenue coming via mobile devices. But it is a much harder product to deliver. A social stream can buffer. A live casino stream cannot. Every hand, spin and deal has to stay synchronised across devices, markets and connection speeds, with no ambiguity over the outcome.

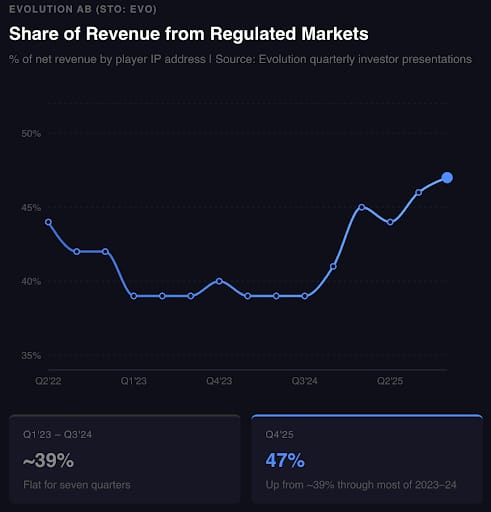

As governments move to capture tax revenue and prevent offshore leakage, the global market is shifting from the unregulated “Wild West” towards formal, licensed frameworks. In the near term, that transition creates friction. New regulated markets bring local licensing, tighter compliance demands and higher operating costs before revenues have fully scaled. The shift is still in its early stages: only seven U.S. states currently have operational iGaming markets, while countries such as New Zealand are only now establishing licensing systems. Over time, however, this should favour scaled, well-capitalised suppliers like Evolution.

On a player-IP basis, regulated play reached 47% of Q4 2025 revenue, up from roughly 39-41% in prior quarters. Source: Evolution

The Moat

Evolution has spent nearly two decades building live casino infrastructure. Hardware, software, video, people and data all have to work together in real time. The company built its own video coding technology to keep streams stable across devices and connection speeds.

That infrastructure is backed by process and trust. Mission Control Rooms monitor operations around the clock. A legal and compliance team of roughly 130 people works across regulated markets. The result was 99.96% system availability in 2024, excluding scheduled maintenance.

Much of Evolution’s production is based in lower-cost operating hubs, while it earns revenue from licensed operators in regulated jurisdictions. That model has helped sustain EBITDA margins above 65%. Even in a tougher 2025, Evolution generated about €1.26 billion of operating cash flow and ended the year with €818 million of cash and a net cash balance sheet.

The operator base creates a flywheel. More operators mean more pooled demand, which supports more native-speaking dealers, better localised tables, stronger peak-time coverage and more dedicated capacity, attracting more operators still. Evolution offers dedicated tables, branded environments, VIP services and native-speaking dealers tailored to local markets. A rival can launch a handful of tables, but replicating that system globally is much harder.

Evolution expanded beyond live casino through the acquisition of NetEnt, and later Big Time Gaming and Nolimit City, building a broader portfolio of digital slot brands. Red Tiger came with NetEnt. Together, these assets underpin Evolution’s One Stop Shop: a single integration point that gives operators access to live casino, game shows and RNG content through one back office. RNG, or random number generator content, refers to software-based casino games such as slots rather than live-dealer products. In 2025, RNG accounted for roughly 14% of group revenue, while Evolution’s First Person titles use a “GO LIVE” feature to direct players from RNG games into live tables.

That distribution advantage is reinforced by the product. Much of that edge has been shaped by Chief Product Officer Todd Haushalter, who joined Evolution from MGM in 2015 and helped push the company well beyond standard live tables. Dream Catcher, launched in 2017, helped establish the live game show category. In July 2025, Evolution signed a multi-year exclusive agreement with Hasbro, allowing them to offer Monopoly branded games as well as other titles.

The difficulty of competing in live casino is also showing up elsewhere. On its Q4 2024 earnings call on 25 February 2025, Light & Wonder said it had commenced the process of discontinuing Live Casino operations.

Evolution’s Monopoly Live game show displayed at ICE Barcelona 2026. Source: Thiago Prudencio/SOPA Images/LightRocket via Getty Images

Testing the Walls

A moat only matters if it holds under pressure. Evolution reports geography on two bases: customer location (where the operator is based), and player IP (approximating where the end user is physically located at the time of play). In Asia, cybercrime and unauthorised redistribution have been a persistent drag. On a player-IP basis, Asia revenue was €193.6 million in Q4 2025, down 4.3% year-on-year. However, Evolution reported that Asia returned to "modest growth" in the final quarter of 2025 (up 2.4% quarter-over-quarter), which it attributes to the success of its aggressive technical and legal mitigation efforts.

Tbilisi was described in Evolution’s 2024 annual report as its largest studio hub, and the 2024 strike showed the risk of relying too heavily on one hub. Since then, the company has expanded capacity into Brazil, the Philippines, Romania and New Jersey. That does not eliminate concentration risk, but it does show management broadening the network.

Europe has also come under pressure. On a player-IP basis, revenue in the region was €177.6 million in Q4 2025, down 12.0% year on year. Ring-fencing rules force operators and suppliers to run markets more locally rather than through shared cross-border setups, adding cost and complexity. In the near term, that hurts. Over time, though, it should favour larger suppliers like Evolution, which have more capital, more operational experience and a greater ability to build local studios, hire local teams and meet market-specific regulatory demands.

In December 2024, the UK Gambling Commission opened a review of Evolution Malta Holding Limited’s operating licence after identifying Evolution games on sites accessible from the UK that did not hold a Commission licence. Evolution said it had acted immediately and was cooperating fully. The review remains ongoing. These pressures help explain why the market has de-rated the stock.

Finally, the Black Cube affair. In 2021, a report submitted to New Jersey regulators alleged that Evolution’s games had reached restricted markets. The New Jersey Division of Gaming Enforcement closed its investigation in February 2024 with no further action, and Evolution later said Pennsylvania’s regulator had also closed its review without corrective action. In October 2025, Evolution said discovery had identified Playtech, another major gambling technology supplier, as the client behind the report and that it would move to add Playtech as a defendant. The litigation remains ongoing, and Evolution said in its 2025 year-end report that it is expected to extend through 2026.

The longer-term implication is one of resilience. While these operational "hiccups" weigh on short-term sentiment, they underscore the immense complexity of leading a global market. Evolution’s ability to maintain high margins while absorbing these shocks highlights a formidable advantage.

Evolution’s trailing P/E has compressed sharply from earlier peak levels to around 10x as at 20 March 2026. Source: Waterhouse VC analysis based on Evolution filings, ECB EUR/SEK reference rates and market prices.

The Opportunity

The market has de-rated Evolution from over 50 times earnings in 2020 to roughly 10 times today, yet the company still operates at a 66% EBITDA margin and generated €1.26 billion of operating cash flow in 2025. That discount now sits alongside a new capital-allocation question.

In March 2026, the board proposed no dividend for 2025, departing from its stated framework of distributing at least 50% of net profit annually. The board said a cash dividend was not the best way to currently create long-term shareholder value. What it plans to do with the cash remains an open question.

Evolution shows what the picks-and-shovels model looks like at maturity: a supplier embedded across 800+ operators, generating more than €1 billion a year in cash while the regulatory moat around it deepens.

The companies we focus on sit much earlier on that curve. Evolution is a reminder that distribution matters as much as product. As these businesses scale, they become more strategically relevant to incumbents like Evolution, which has both the reach and the balance sheet to act.